Hydrogen Market Design and Policy

Figure 1. Hydrogen policy framework

What are the economic consequences of the transition to a hydrogen-based economy? What is the role of supportive policies in achieving Qatar’s H2 economy and repositioning it as a global supplier of clean energy? Qatar’s hydrogen market modeling will provide insight into various scenarios mid- and long-term depending on certain inputs and realistic assumptions. This stage will provide the key modeling inputs and assumptions used to develop a global market demand, domestic and export market scenarios for Qatar. The modeling will also include economic and environmental impact analyses for the three scenarios (baseline scenario, target market development scenario, and rapid international market development scenario). The development of Qatar’s export market will be modeled through scenarios of critical infrastructure, technological, and demand sources. The data to be used in the model are a combination of publicly available information, Researchers’ analyses based on multiple public sources, industry knowledge, and current projects. The hydrogen policy framework is displayed in Figure 1.

Multi-sector H2 Supply Chain Mapping Portfolio

Decarbonization and Enhancing Qatar's Energy Mix

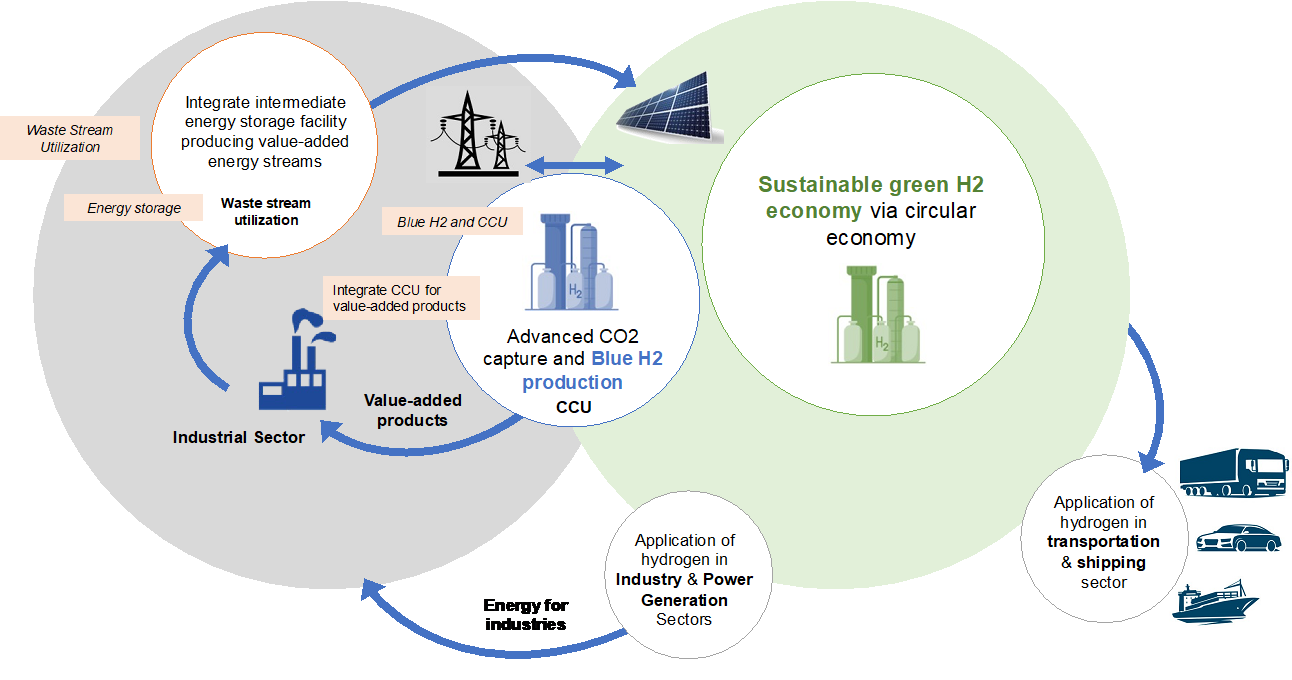

Figure 2. Natural Gas Monetization through H2 & Circular Economy

What will be the role of H2 in enhancing the country's energy mix in its industry, power generation, and global market sectors? Qatar's gas sector could be interested in a comprehensive study to draw the roadmap to the transition to blue H2 and identify the challenges at each stage of the H2 value chain (production/transportation/storage/marketing). The Electricity Sector and their partners may also be interested in how H2 could be introduced in the power generation sector and the necessary modifications and the cost of green electricity. There is a need to determine H2 role in the existing Qatari Industry and the potential to leverage the existing infrastructure considering the following: (1) expand the country’s Gas Monetization supply chains to include large-scale Blue H2 production, (2) study the realistic impacts on industrial sector decarbonization, and (3) opportunities of using H2 carriers to transport H2 to global markets, see Figure 2. The Large scale deployment of Blue H2 may potentially contribute to the emissions reduction target of 64.7 MtCO2 eq in the oil and gas sector by 2030. And for that primary reason, key stakeholders are likely interested in blue hydrogen in the short and medium terms to strategically follow the international market trends

Global leaders and all the signatories to the United Nations Framework Convention on Climate Change (UNFCC), who participated in the COP26 summit in Glasgow, agreed to accelerate decarbonization of cities and industries in order to keep global temperatures well below 2 °C above preindustrial levels and to pursue efforts to limit global warming to 1.5 °C (National Grid, 2021; UNCCC, 2021). Hence, there is global interest (short-term) in decarbonization of industrial, power generation, transporation, and shipping sectors, to reduce the environmental impacts of high per capita CO2 emissions and to meet global commitments for environmental sustainability. There is a need to determine the major sources of CO2 emissions and develop mitigation and CO2 management plans for these sectors. The mitigation could involve proposals for CO2 reduction through process optimization, CO2 utilization, and sequestration in the industrial sector. Long-term plans for energy transformation could focus on green and blue hydrogen. Here, policies, technologies, and a roadmap for the gradual introduction of H2 in the energy mix would be great importance.

H2 Production, Transportation and Storage Challenges Portfolio

Integrating H2 into the existing Natural Gas Infrastructure: Short and Midterm Range

Figure 3 Hydrogen transportation value chain (A.K. Sleiti and W. A. Al-Ammari, 2022)

What is the feasibility of making Qatar a hydrogen hub by 2070? Several challenges need to be addressed to make Qatar an H2 hub by 2070. These challenges include repurposing existing NG infrastructure to handle H2 and mixtures, developing more efficient precooling and liquefaction processes and refrigerants, developing new combustion technologies for H2 and mixtures, innovative storage and transport technologies, and reducing boil-off losses. The focus is on developing large-scale H2 liquefaction technology to achieve breakthroughs in liquefaction costs and energy efficiency and to develop new oil-free centrifugal compression technology. The empahsis will also be on the feasibility of using existing oil and gas infrastructure for H2 transportation (see Figure 3), shipping scale-up H2 tank designs and boil-off lose solutions, H2 combustion using existing and new technologies, and H2 storage technologies.